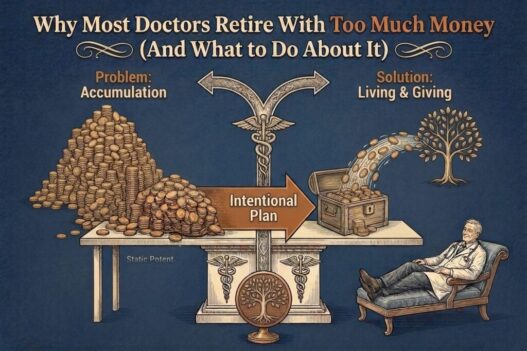

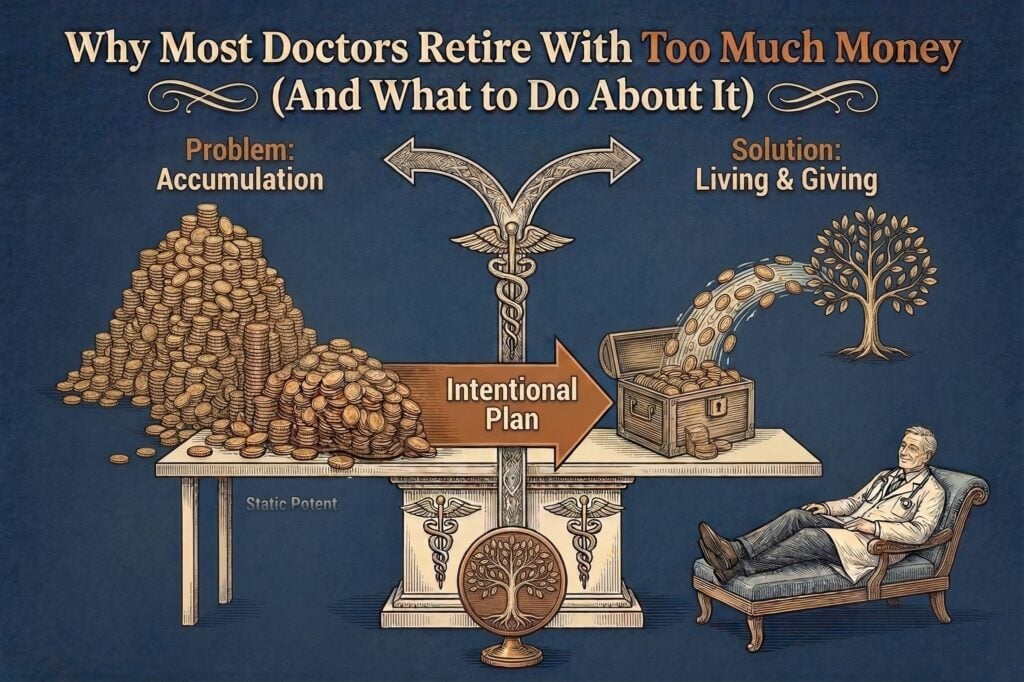

Physician conversations around money and saving almost always circle back to how doctors are notoriously spendthrift and “bad” with money. After all, one-in-four doctors hit their mid-60s without even a million dollars to show for three decades of attending-level income.

That factoid, while appalling, is also slightly dated (from 2019). There's a flip side to it that gets almost no airtime.

Source: Medscape

A growing number of physicians are shuffling off this mortal coil with a small fortune they never touched. They worked past the point of financial necessity, delayed trips they never got around to taking, and spent the last years of a productive life quietly hoarding a nest egg that their kids or the IRS will end up carving up.

That could be categorized as a different kind of failure altogether.

In case you missed it: Are You Really Wealthy? A Data‑Driven Look at How High Earners Undervalue Their Net Worth

Running Out the Clock After the Game is Already Won

According to Medscape's Physician Retirement Survey, the average physician expects to need $4.01 million to retire comfortably. Men say $4.27 million, while women say $3.57 million. That's a reasonable target.

Multiply your annual spending by 25, add a buffer for healthcare, and you have a number. Most attendings who stay financially disciplined through their peak earning years will get there. Many will blow right past it.

Source: Medscape

At retirement age (60–70 years old), somewhere between 15% and 22% of physicians have a net worth above $5 million. That group is not exactly stretched thin. And yet plenty of them are still showing up at the clinic.

Based on survey data from the AMA Insurance Agency, 58% of physicians retire after age 65, compared to men in the general U.S. workforce who typically retire between 62 and 64. Doctors work later than almost anyone, even when their savings stopped requiring it years ago.

Research on the 4% withdrawal guideline shows that most of the time, a retiree following conventional withdrawal wisdom will die with many multiples of what they started out with. For physicians with above-average portfolios and below-average spending rates in retirement, the number can be even more dramatic.

The nest egg keeps growing, yet…the doctor keeps working.

Learn more about The Ideal Level of Wealth

“One More Year” Is a Trap

Ask any physician who delayed retirement why they did it, and you will hear variations of the same answer: not quite yet, want a bigger cushion, one more good year.

Among physicians who delay retirement, common reasons include concern for patients, a lack of interests outside medicine, financial obligations, and a fear of losing their sense of identity.

That last one is worth mulling over. Identity is doing a lot of heavy lifting in that list. Medicine has a way of colonizing a person's sense of self. Physicians often find it difficult to separate themselves from their work.

For many, being a physician is who they are. Period. When the job is also the person, retirement feels more like an amputation than a chance to relax.

The financial justification is often a cover story. According to CompHealth's Survey on Physician Views on Retirement, the three most common reasons (PDF) physicians plan to work beyond 65 are enjoyment of the practice of medicine, the social aspects of work, and a desire to maintain their existing lifestyle. Fair enough.

But enjoyment and necessity are different things, and conflating them can be costly.

74% of physicians who want to retire cite burnout as a reason, while 61% want time to pursue other passions, and 45% want more time with family.

Those are far from vague, hypothetical desires. They are specific losses that are accumulating every year a doctor spends in a system that, by most accounts, is not getting any gentler.

Source: Medscape

The average age of active physicians in 2025 is 54.4, according to data from Definitive Healthcare covering over 810,000 physicians.

That's well above the national workforce median of 41.8. These are not people in the early innings of a career. A lot of them are simply running out the clock.

Also read: Why Do Americans Work So Much?

The Scarcity Mindset Doesn't Retire With You

Part of what makes this hard is psychological and has nothing to do with spreadsheets.

Decades of building wealth create a one-way muscle. Money goes in. The account grows. That is the entire plan for 30 years. Then retirement arrives, and suddenly the rules invert. Money is supposed to come out? For someone who has spent their adult life as an accumulator, that shift can feel almost physically wrong.

Financial professionals who work with high-net-worth retirees have a name for the reluctance to spend in retirement: the decumulation problem. It takes considerable training and discipline to reverse the saving habit after decades of using it to build wealth.

This mindset is understandable, but it's also a slow contamination of quality of life. The physician who has spent 30 years clearing every financial hurdle, like paying off student loans, putting kids through school, and clearing that mortgage, often finds a new hurdle to clear. The goal posts move.

Physicians had funded about 77% of their desired retirement amount at the time they were surveyed, which sounds like near-miss territory. But for a large chunk of that group, the gap between “funded” and “desired” translates to anxiety that no dollar figure will ever fully close.

Chad Chubb, founder and certified financial planner at WealthKeel, has seen it up close. “It is the balancing act of having their income multiply overnight, while juggling large student loan debt, starting a family, buying a home, and being a great physician,” he says.

The habits that form during that pressure-packed early attending phase (save aggressively, spend cautiously, always protect the downside) do not automatically dissolve once the account balance looks comfortable. For many physicians, those habits harden into a permanent orientation toward scarcity that no amount of wealth can cure.

Read: The Physician's Guide to a Regret-Free Retirement: Three Steps to Financial Freedom

What You Think You Need vs. What You Actually Need

Is physician retirement really as complicated as everyone makes it out to be?

The 4% rule, while not a perfect withdrawal method, serves as a useful rule of thumb. Multiply what you spend annually by 25, and you have a rough retirement number. For most physicians, that works out to somewhere between $1 million and $5 million, depending on lifestyle.

A few things reduce that number in practice. Physicians who earned above the Social Security wage base for most of their careers can expect close to the maximum benefit of $4,152 (for 2026) per month at full retirement age, which is about $49,800 per year. For a couple where both spouses worked, that figure roughly doubles.

That's almost $1 million per year in lifetime benefits that do not need to come out of a personal portfolio.

Then comes the spending itself. The assumption that retirement requires replicating an attending physician's spending level is almost always wrong. The mortgage is likely to be paid off.

The kids are out of the house. Malpractice premiums are gone. CME costs, licensing fees, and disability insurance premiums — all of it disappears. Many physicians discover, with some surprise, that retirement costs significantly less than their working life ever did.

A physician saving 20% of a $363,000 salary and earning a 5% real return over 30 years should accumulate roughly $4.8 million in their nest egg, and that's before you factor in home equity, savings outside retirement accounts, or Social Security.

Run that forward on a higher-earning specialty and the numbers get considerably larger.

I am, by no means, trying to say that saving is bad. I'm just pointing out that most physicians who follow a basic financial plan for a full career are going to land in comfortable territory without needing to squeeze out three more years of work.

Learn more: The Top Retirement Questions Physicians Need to Ask

The Go-Go Years

There is a window in early retirement (roughly from 60 to 75) when most people have the energy, health, and desire to do everything they said they would do once they stopped working. Researchers and financial planners call these the “go-go years.”

After that comes the slow-go phase. Then the no-go phase. The spending bucket shrinks in each.

There's plenty of time in your 80s to sit in front of the TV. Your 60s are for living.

But that window is finite, and it does not automatically wait while a doctor finishes one more contract cycle. A physician who retires at 68 instead of 63 has traded five go-go years, arguably the highest-value years on the retirement calendar, for a portfolio that is already larger than it needs to be.

Maybe that's morbid. But it's also an argument in favor of optimization. Nearly 50% of physicians in their 40s say they want to retire in their 50s or early 60s.

Happiness Costs Less Than You Think (Even In Retirement)

When Too Much Is the Wrong Problem to Have

None of this means physicians should blow their savings on lifestyle inflation the moment they hit their number. The tail risks of that are disastrous.

Long-term care can run upwards of $12,000 per month for a quality facility. Healthcare costs in early retirement, before Medicare kicks in, can gut a poorly structured withdrawal plan faster than most people expect.

Kids, aging parents, and the general unpredictability of a 30-year retirement all warrant a cushion.

But a cushion and a fortress are different things. A physician with a $6 million portfolio, no mortgage, and Social Security on deck is not walking a financial tightrope. They are statistically very likely to die richer than when they retired.

In that scenario, worrying about the money is superfluous. Better to think about whether the years are being well spent.

26% of physicians reported being “not very” or “not at all” confident that retirement would be rewarding. Confidence in retirement is not just a financial variable. It carries over into relationships, purpose, structure, and identity. All of which do not require a hospital badge to access.

Physicians who delay retirement indefinitely because they cannot picture life on the other side are trying to outrun a reckoning. Or trying to conserve meaning in some misguided way. But stacking on extra years is a poor substitute.

Also read: Building Retirement Income Streams as a Physician: Strategies and Tactics

What To Do About It

Knowing you have more than you need is the easy part. Doing something constructive with that knowledge — without torching your financial security or watching the IRS take a disproportionate cut — is where the real work begins.

Give It Away — With a Tax Code Cherry On Top

Charitable giving is not just good karma for physicians with oversized nest eggs. Structured correctly, it is one of the most tax-efficient moves available in retirement.

The most direct tool is the Qualified Charitable Distribution. A QCD allows individuals who are 70 1⁄2 or older to donate up to $111,000 directly from a taxable IRA to one or more charities, satisfying all or part of their required minimum distribution while keeping the distribution out of their taxable income entirely.

For a physician with a heavily loaded traditional IRA generating large RMDs they do not need, this can be very helpful. Because the QCD amount is excluded from adjusted gross income, it can also reduce exposure to higher Medicare premiums and the taxation of Social Security benefits — both of which are income-sensitive.

A married couple where both spouses have IRAs can direct up to $222,000 per year to charity this way without it counting as income, meaningfully reducing their tax exposure.

If the charitable impulse is there but the specific recipients are not yet decided, a Donor-Advised Fund does the job.

A DAF allows a donor to contribute a large sum in the current year, receive an immediate income-tax deduction, and then recommend grants to specific charities over time, all while the contributed funds grow tax-free in the interim.

For physicians who regularly itemize, donating appreciated securities directly to a DAF rather than selling them first generally eliminates the capital gains tax that would otherwise be owed, and still generates a deduction for the full fair market value of the donated assets.

Physicians sitting on appreciated index fund positions built up over three decades have a lot of room to work with here.

Important: Starting in 2026, under the One Big Beautiful Bill Act, QCDs are actually more attractive than before. While charitable deductions for itemizers now face a new 0.5% AGI floor and a reduced benefit for top-bracket taxpayers, QCDs are excluded from income entirely and are unaffected by these limits.

Of course, you should still run it by a CPA before pulling the trigger.

One Big Beautiful Bill Act: What It Means for Physician Taxes in 2025 and 2026

Get Serious About Spending Down

Nearly half of all retirees have no formal withdrawal strategy, choosing instead to take money out as needs arise rather than following any consistent decumulation plan. For the general population, that is a problem because it risks running short.

For physicians with a portfolio that outpaces their spending, the opposite is true. The money just keeps piling up, the RMDs hit in their 70s, and suddenly a physician who lived frugally for decades is getting pushed into the top bracket against their will.

What you need is a written decumulation plan. An intentional, structured approach to withdrawing retirement assets that matches spending to available resources. The bucket strategy, originally developed by financial planner Harold Evensky, is one of the more intuitive frameworks.

The approach divides a portfolio into three separate buckets: short-term liquid assets to cover near-term expenses, moderate-risk holdings for the intermediate horizon, and a long-term growth bucket that can afford to ride out market swings.

The practical benefit for physicians is as psychological as it is financial. A doctor who knows their next three to five years of expenses are sitting in low-risk assets is far more likely to actually spend the growth bucket as intended, rather than watching the whole portfolio compound indefinitely while they live off Social Security and practice income.

We don't want to drain the tank outright. But it's important to let yourself use the money you've earned.

Front-Load the Next Generation's Education

Those who are uncomfortable spending on themselves often find it easier to deploy capital when the beneficiary is a grandchild.

The 529 superfunding strategy gives them a clean legal mechanism to do exactly that. Under the 5-year gift tax averaging provision, an individual can contribute up to $95,000 to a single beneficiary's 529 plan in one year (or $190,000 for a married couple filing jointly) and spread the gift tax treatment across five years without touching the lifetime exemption.

A physician couple with four grandchildren could move $760,000 out of their taxable estate in a single transaction, with the funds growing tax-free for education.

Done at the right time, the compounding alone makes a material difference. An $80,000 lump-sum contribution compounded at 8% over 18 years grows to roughly $319,000, compared to about $292,000 if that same amount is spread out over 5 years in smaller installments.

Earlier is better, and IRS Form 709 is required to make the election, but no gift tax is actually owed as long as contributions stay within the five-year limit per beneficiary.

Learn more: How to Fund a 529 Plan in 2025: Complete Guide for Physicians and Families

The Roth Conversion and the RMD Clock

This one is about keeping more of what you make out of the government's hands. Physicians who retire with seven-figure traditional IRAs and 401(k)s are staring down a tax time bomb.

RMDs kick in at 73 (or 75 for those born in 1960 or later) and scale upward each year based on account balance and life expectancy. For a physician whose portfolio continues to grow in early retirement, that can mean distributions well above actual spending needs. Inadvertently pushing them back into high brackets at exactly the age they thought they were done earning high income.

The window between retirement and age 73 is when Roth conversions are cheapest. Income drops, brackets open up, and the conversion can be done at a rate meaningfully below what the RMD would eventually impose.

The numbers vary by individual situation and warrant a proper analysis with a tax professional, but the general principle is sound: pay the tax now at a known rate rather than later at an unknown (and possibly higher) one. Converted Roth assets also pass to heirs income-tax-free, which, for a physician who has already outrun their own spending needs, turns estate planning from a liability into a gift.

Backdoor Roth vs Taxable Investing for High Earners

Fly Business Class

This one is a reminder that the purpose of building wealth was never the wealth itself. And I know, after years of living frugally, it sounds diabolical. But hear me out.

Or rather, Christine Benz, Director of Personal Finance and Retirement Planning at Morningstar, who says: “There's so much that's suboptimal about the way we approach retirement. Especially for people who are getting ready to retire because, you know, you're effectively sending people out and saying, ‘here's your savings, figure it out.'”

The physicians most likely to die over-saved are often the same ones who kept telling themselves they would travel more, do more, live more…just not yet.

William Bengen, the creator of the 4% rule, now argues that a 4.7% withdrawal rate may be appropriate for many retirees, and he personally spends more than that in his own retirement. A physician at 66 who decides to spend another $30,000 a year on experiences they have been deferring is using their retirement for the very thing it was meant for.

None of this means you have to give in to recklessness. It just calls for some honesty about what the numbers actually say, and enough self-awareness to notice when the accumulation habit has outlived its usefulness.

The physician who worked 30 years to build a $6 million portfolio did something genuinely hard. The harder thing, it turns out, is trusting that it is enough, and then actually living like it is.

In case you missed it: Why Do High Earners Struggle to Feel Rich

Getting It Right

So what does a well-calibrated exit actually look like?

It starts with a real number, not some vague aspiration.

Run the 4% calculation against your actual projected retirement spending. Add Social Security. Subtract the costs that disappear when you stop practicing. If the numbers make sense, you're good to go. A target that keeps moving is not a target.

About 48% of physicians plan to wait until age 70 to claim Social Security, capturing the maximum delayed credit. For healthy physicians with substantial investment assets, that is generally smart.

But it also assumes those physicians will actually retire in time to make the bridge period work. A physician who keeps working until 70 and then claims Social Security has left the delayed-claiming benefit on the table.

Finally — and this one is underrated — build a retirement identity before retirement arrives. Physicians who struggle with the transition often cite a lack of interests outside of medicine and a fear of losing their sense of self as primary obstacles. More money won't solve that. More life just might. This should be built in parallel to your career, so that walking out of the hospital for the last time feels like walking toward something rather than away from it.

The irony in all of this is that physicians are uniquely positioned to retire well. They earn more, they save at higher rates when they try, and they have access to tax-advantaged accounts most Americans cannot touch. The infrastructure is there. What often gets in the way is the belief that no number is ever quite enough.

And if I may be so bold as to say: you do not need a bucket list. Or a five-year plan for your retirement years, or a portfolio of hobbies, or a second act that proves the time was well spent. The idea that retirement must be optimized, or productive, in order to be justified, is frankly — bogus.

There is a kind of peace in doing nothing that most physicians have not tasted since before residency. No scrolling. No charting. No optimizing. Just a Tuesday afternoon with nowhere to be and no obligation pulling you away. If that's not nostalgic, I don't know what is.

If you are old enough to remember being bored before smartphones took over our every waking moment, you remember what that felt like. The particular quality of a slow hour that belonged entirely to you. Retirement might be the last real chance to get that back before it disappears from the human experience altogether.

For many of us, that just might be the whole point.

Frequently Asked Questions

Do doctors really retire with too much money?

More than people talk about, yes. Research on the 4% withdrawal rule consistently shows that the average retiree following conventional withdrawal wisdom ends up with many multiples of their original nest egg by the end of a 30-year retirement. For physicians with above-average portfolios and below-average spending in retirement, the compounding effect is even more dramatic. The nest egg keeps growing long after it needed to stop. The uncomfortable irony is that the same financial discipline that built the wealth often prevents them from ever using it.

How much money does a physician need to retire comfortably?

According to Medscape's Physician Retirement Survey, the average physician puts their retirement target at $4.01 million. That figure varies by gender and specialty, but the math behind it is straightforward enough. Estimate what you actually plan to spend each year in retirement, multiply that number by 25, subtract guaranteed income sources like Social Security, and you have your working target. For a physician couple both claiming Social Security, that guaranteed income alone can account for a significant portion of their annual spending, which means the personal portfolio requirement drops considerably from what most physicians assume.

What is the decumulation problem and why does it affect physicians?

Decumulation is the process of systematically drawing down retirement assets rather than continuing to accumulate them. After 30 years of building a one-way financial muscle, many physicians find the reversal psychologically difficult. Money was always supposed to go in. Seeing it come out triggers the same anxiety that got them saving in the first place, even when the numbers say there is no reason for it. The habits that protected them during their accumulation years calcify. No account balance, no matter how large, automatically dissolves them.

Why do so many doctors delay retirement even after reaching financial independence?

The reasons are rarely as financial as they appear. According to CompHealth's Survey on Physician Views on Retirement, the most commonly cited reasons physicians plan to work past 65 are enjoyment of the profession, the social structure work provides, and a desire to maintain their lifestyle. Identity is the undercurrent running through all of it. Medicine does not just provide income. For many physicians, it provides the entire architecture of meaning, social connection, and daily structure. Removing it without something to fill the space is what makes retirement feel threatening, not the balance sheet.

What are the go-go years in retirement?

The go-go years are the early phase of retirement, generally from the mid-60s to the mid-70s, when most retirees have the health, energy, and desire to actually do what they spent decades planning to do. After that comes the slow-go phase, where physical limitations start narrowing the options, and eventually the no-go phase. Discretionary spending typically drops in each successive phase. A physician who delays retirement by five years past the point of financial independence does not just lose five years of work. They trade five go-go years for a portfolio that was already larger than necessary.

What is a Qualified Charitable Distribution and how does it reduce taxes in retirement?

A QCD allows anyone aged 70½ or older to transfer up to $111,000 per year directly from a traditional IRA to a qualifying charity. That amount counts toward the required minimum distribution for the year but is completely excluded from taxable income. For a physician with a heavily loaded IRA generating RMDs they do not actually need, this is one of the cleanest available tools. It reduces adjusted gross income, lowers Medicare premium exposure, keeps Social Security benefits from being taxed at a higher rate, and directs excess wealth toward causes that matter. Married couples with separate IRAs can each use the provision, doubling the annual ceiling to $222,000.

What is 529 superfunding and is it worth it for physicians?

Superfunding uses a provision called 5-year gift tax averaging to let a grandparent or parent front-load a child or grandchild's college savings account in a single year. In 2025, an individual can contribute up to $95,000 per beneficiary, or $190,000 for a married couple, and elect to spread the gift tax treatment across five years without touching the lifetime exemption. The money then grows tax-free inside the 529. For a physician couple with multiple grandchildren, this is one of the more efficient ways to move a meaningful sum out of a taxable estate while doing something useful with it. Earlier contributions compound longer and produce materially better outcomes than the same amount spread over time.

When should a physician do Roth conversions?

The window between retirement and age 73 is typically the cheapest time to convert traditional IRA or 401(k) funds to Roth. Earned income has stopped, Social Security may not have started, and required minimum distributions have not yet begun pushing adjusted gross income upward. That combination usually places a retired physician in the lowest tax brackets they will occupy for the rest of their lives. Converting during that window means paying tax at today's known rate rather than a future rate that RMDs may force even higher. Converted Roth assets also pass to heirs income-tax-free, making it a useful tool for physicians who have already outrun their own retirement spending needs.

Is it bad to save too much for retirement?

The saving itself is never the problem. The problem shows up when accumulation becomes reflexive rather than intentional, and when a number that was always supposed to be a finish line keeps getting moved. A physician who has hit their target, runs a solid withdrawal plan, holds a reasonable cushion for healthcare and long-term care, and is still not spending has crossed from prudent into something else. At some point, excess wealth is no longer serving the physician. It is just sitting there, growing, waiting to be inherited or taxed, while the years it was meant to fund quietly pass.

What are the biggest financial mistakes physicians make in retirement?

The most common one is not spending. Physicians who spent decades mastering the accumulation phase often arrive at retirement with no plan for the other side. They take money out only as needs arise, watch RMDs push them into unexpected tax brackets in their 70s, and leave a heavily weighted traditional IRA to heirs who will owe income tax on every dollar. A close second is holding off on Social Security too long without actually retiring, which eliminates most of the benefit of the delay strategy. And third is treating retirement as a financial problem to be solved rather than a phase of life to be lived, which leads to the “one more year” trap that steals the go-go years one contract cycle at a time.