As of 2025, among new medical school graduates who carry debt, the typical student debt burden is around $216,659. And that's just for med school alone. When we add in undergraduate loans, the average total rises to approximately $246,659.

These numbers matter more now than ever because federally backed student loan policy is tilting beneath the feet of aspiring physicians.

A recently enacted federal spending bill imposes a $200,000 lifetime cap on borrowing for professional degrees and ends the Grad PLUS program for new borrowers. That caps much of what future med students can borrow under federal safety nets.

The average debt number is a potential ceiling for many entering the profession. Let's break down how who carries more or less debt, how doctors pay it off, and how refinancing, forgiveness, and policy shifts change everything.

Average Student Debt Owed by Doctors

Medical education is an eight-year investment if you count the typical undergraduate pre-med path plus four years of medical school, but many physicians accrue debt even earlier.

Roughly 70% of medical graduates have education loan debt, and 74% of practicing physicians originally borrowed to get through medical school. Among physician borrowers, about 32% still owe more than $250,000.

Among the class of 2024, the average indebted graduate owed about $212,341, and 84% of that class carried at least $100,000 in total education debt. A significant percentage of graduates owe between $200K and $300K (33%), and a meaningful subset exceeds $300K (23%).

These numbers matter because they interact with specialty income expectations, family formation, home mortgages, and the willingness to take lower-paying but socially essential jobs.

The historical perspective is sobering to say the least.

From 1978 to 2025, average medical school debt increased by roughly 1,505% in nominal terms, growing far faster than general inflation.

The cost of attendance for a four-year program varies widely between public and private institutions, but 2025 estimates place median COA well into the mid-six-figures over the course of a degree once you include living expenses.

Find out What It Actually Takes to Eliminate Debt

Public vs. Private Med Schools

The shorthand that private medical schools cost more remains true, but the story doesn't end there.

In 2024, 73% of public medical school graduates borrowed, and 67% of private school graduates borrowed, with the average debt among borrowers from public schools around $203,606 and among private-school borrowers around $227,839.

What that means is simply that private schools carry higher sticker prices, but institutional grants, pre-existing family resources, scholarship mixes, and the geographic mix of students shape who borrows and how much.

Institutional variation is dramatic. Some public institutions report average indebtedness in the $120K–$190K range for graduates who borrow, while the number can be even lower than six figures.

Some private schools, on the other hand, report averages in the ballpark of $250K and up.

A table of specific institutions' average indebtedness (University of California system schools versus Northeastern private schools, for instance) reads like a map of economic choices with implications for debt load later in life.

| University of California Schools | Northeastern Private Schools | ||||||||||||||||||||||||||

|

|

Student Debt by Specialty

If you want to see how student debt shapes outcomes, look at specialties. Specialty choice is no longer just what interests you, plus the fate of the Match. The new equation factors in debt math, too.

Physician salaries and debt interact unevenly across the specialty spectrum, as evidenced by Medscape's physician compensation surveys, which consistently show that primary care incomes are lower than in other specialties.

Yet, debt burdens hover in overlapping ranges. Here's a breakdown according to the AMA:

Family medicine/primary care physicians

Typical indebtedness falls in the neighborhood of $180,000–$220,000. Training length is shorter (3 years), but income is lower on average (~$265K to $280K depending on subspecialty and geography), which stretches the debt burden relative to income.

Emergency medicine

Debt commonly lands around $200,000. Shift work and opportunities to moonlight can accelerate repayment, but burnout and lifestyle tradeoffs apply.

Orthopedic surgery

Median indebtedness around $190,000. The training is long (5 years), which amplifies interest accrual during low-pay years.

Psychiatry

Median debt is about $190,000, with 27% of graduates owing $200,000 or more. Psychiatry's four-year residency plus mid-range compensation ($341K) means slower deleveraging than procedural fields. So, hospital or health-system roles that offer loan repayment are common career choices.

Pathology

Median debt sits around $185,539, with 23% of graduates owing $200,000 or more. Pathology's training and typical employment mix (academic and hospital work) make institutional repayment programs and PSLF-eligible roles an important part of many early-career plans.

The practical upshot is that debt nudges students toward higher-paying specialties and institutionally supported employment models (hospital employment and private equity–backed platforms) and away from lower-paying, high-need areas such as rural primary care, academic medicine in underserved regions, or public health.

How Long Does it Take for Physicians to Pay Off Student Debt?

Physicians are sometimes painted as uniformly wealthy, but that narrative neglects the timing. Most doctors don't hit true attending's pay until their 30s. So when you combine delayed high income with interest compounding and you have a wide spectrum of payoff timelines.

On average, it takes 13 to 20 years for a typical physician who uses income-driven repayment (IDR) at least during training and does not receive wholesale forgiveness to pay off their student loans.

A subset of physicians aggressively pursue debt freedom (paying off in 5 to 7 years post-training), but those are the exception, as it involves moonlighting, substantial bonuses, and rigorous lifestyle discipline generally to achieve.

For many, the age at which they gain freedom from debt is somewhere in the mid-40s to early 50s, though variation is large.

Those who pursue PSLF and complete 120 qualifying payments while in eligible employment can be debt-free earlier in calendar years (10 years of qualifying payments), but PSLF has its own administrative and eligibility pitfalls.

Debt Repayment Strategies for Physicians

For most physicians, medical school debt defines the first decade of financial life.

A $200,000 to $300,000 loan balance can dictate where you live, what kind of medicine you practice, and even when you start a family.

Fortunately, there isn't just one way to pay it down. Repayment strategies differ as widely as medical specialties, and the smartest approach depends on your debt-to-income ratio, career path, and long-term goals.

Public Service Loan Forgiveness (PSLF)

For doctors who plan to stay in the nonprofit ecosystem, like academic medicine, university hospitals, or public hospitals, Public Service Loan Forgiveness (PSLF) remains the gold standard.

The program wipes out the remaining federal loan balance tax-free after 120 qualifying payments made while working full-time for a qualifying employer. That's typically 10 years of service.

But PSLF isn't a free-for-all. To qualify, your loans must be Direct Federal Loans, and you must be enrolled in an income-based repayment (IBR) or income-driven (IDR) plan. Hospitals owned by private equity or for-profit groups don't qualify, so if you're headed into private practice or a lucrative surgical subspecialty, PSLF likely won't apply.

The savings, however, can be enormous.

Physicians carrying large balances can see six figures forgiven. Still, PSLF demands consistency. Payments must be certified and tracked through a federal loan servicer. Missing documentation or working part-time can set you back years.

There's a cautionary note: consolidating existing federal loans midway through PSLF resets your qualifying payments to zero. So if you're already several years into repayment, consolidate only if you're sure it's necessary.

For those not pursuing federal forgiveness, it's worth exploring state-specific loan repayment programs. Several states offer medical student loan repayment awards of $20,000 or more per year for physicians who practice in rural or underserved regions.

Learn more about PSLF For Doctors: Is It Still Worth It?

Income-Driven Repayment (IDR) Plans

Income-driven repayment plans are the workhorse of physician debt management.

Even if you're not eligible for PSLF, IDR allows you to scale monthly payments to your income (typically 10% of discretionary income) while maintaining eligibility for forgiveness after 20 to 25 years.

Different plans differ in nuance, but the principle is the same: align payments with earning potential in early-career years, then ramp up contributions later as your salary climbs.

The catch is tax exposure. Unlike PSLF, forgiveness through IDR is taxable under current law. That means the forgiven balance in year 20 could trigger a substantial tax bill. Financial planners often advise setting aside a portion of savings each year to cover this future “tax bomb.”

As federal legislation evolves, repayment rules continue to shift. Staying current with updates from the Department of Education can help you navigate plan transitions.

Private Loan Refinancing

When PSLF isn't in the picture, private loan refinancing can make a dramatic difference. This strategy involves converting federal loans into private bank loans, typically at a lower interest rate and with flexible repayment options.

A physician with a $250,000 balance at 6.5% who refinances to 4.2% could save tens of thousands over the loan's life.

Private refinancing can also be repeated whenever rates fall, which helps high earners keep pace with market trends.

That said, the move is irreversible. Once your federal loans are refinanced, you lose access to IDR and forgiveness programs for good.

Many new attendings make this mistake too early, before their income stabilizes or before deciding whether they'll work in a qualifying nonprofit. The prudent move is to wait until you're certain of your long-term career path before refinancing.

You could lower your student loan interest rate and put up $500 towards your new loan with Earnest. Check your rate in just 2 minutes.

Other Things to Consider

Some physicians prefer to play the long game by minimizing required loan payments to free up cash flow for investing.

Under IDR, lower monthly payments can create breathing room for retirement contributions, index funds, or real estate ventures.

If your average return on investment exceeds your loan interest rate, this can be a mathematically sound strategy.

For example, investing in a diversified portfolio returning 7% annually while paying 5% loan interest yields a net gain over time. But that assumes discipline, consistency, and the stomach for market volatility.

If debt feels psychologically suffocating, or if high interest rates aren't on your side, paying off loans faster remains the sounder emotional and financial move.

A growing number of early-career physicians are using locum tenens or per diem work to accelerate loan repayment. Data shows that full-time locum physicians earn roughly $32.45 per hour more than their permanent counterparts. That income differential can easily translate into a king's ransom per year in additional payments toward principal.

Interestingly, this approach doesn't always require travel. 38% of locum physicians report taking short-term assignments close to home. For new graduates still testing different practice models or those seeking schedule flexibility, locum work can become both a financial and lifestyle hedge.

The best repayment plan isn't purely mathematical; it's situational.

A psychiatrist earning $340,000 with a $190,000 debt load might find IDR or PSLF optimal.

A pathologist earning $260,000 with $185,000 in loans could be better off refinancing and paying down aggressively.

The calculus depends on your specialty's income trajectory, your tolerance for debt, and your vision for work-life balance.

In every case, run the numbers, then run them again with a financial advisor who understands physician finances. Because, ultimately, student loans aren't just liabilities, they're the opening act of your financial story.

When Refinancing Makes Sense and When It's a Trap

Refinancing private loans or refinancing federal loans into private loans is not a neutral decision. The financial upside is that you get lower rates, fewer servicers, and the chance to pay far less interest.

For an attending with high disposable income and no intention of pursuing PSLF, refinancing usually pays off.

But refinanced federal loans forfeit income-driven options, PSLF eligibility, death/disability discharge protections, and generous forbearance options.

During economic shocks (pandemic, job loss, illness), federal programs frequently provide materially better relief than private servicers.

If you refinance and later pivot to a nonprofit job seeking PSLF, you can't step back into federal protections without refinancing again, and scrapping a private loan back into federal programs is usually impossible.

Below is a table with the pros and cons of refinancing:

| Pros of Refinancing | Cons/Risks of Refinancing |

| Lower interest rates can potentially save you tens of thousands. | Refinanced loans are no longer eligible for Public Service Loan Forgiveness (PSLF). |

| Simplifies finances by consolidating multiple loans into a single monthly payment. | You lose access to income-driven repayment (IDR) and other federal forgiveness programs. |

| Many lenders offer cash-back bonuses and promotional incentives for refinancing. | Federal benefits like the pandemic-era REPAYE interest subsidies and temporary forbearance programs no longer apply. |

| Flexibility to choose among different loan terms like shorter terms for faster payoff, longer terms for lower payments. | Payments are no longer tied to income, which can strain cash flow during early-career years. |

| Improved customer service and streamlined loan management through private lenders. | Less protection in cases of death or disability, since private lenders set their own policies. |

| A strong credit profile or cosigner can help secure lower rates and better terms. | Some borrowers may need a cosigner, and qualification depends on creditworthiness. |

| Removing a cosigner later can improve financial independence. | Shorter forbearance windows and fewer hardship protections compared to federal loans. |

| Variable-rate loans can reduce interest costs in a falling-rate environment. | Variable rates can also increase over time, raising long-term costs. |

| Faster payoff potential for borrowers committed to aggressive repayment. | No automatic grace period after graduation or during transition periods. |

| Freedom from federal policy uncertainty, hence no legislative risk. | Once refinanced, federal loans cannot be converted back. |

If you are a resident, do not refinance federal loans unless you are sure you will never need federal options; if you are an attending, run the numbers.

If you are certain your career trajectory avoids PSLF, refinancing is worth a close look.

How Debt Reshapes Physician Careers and Lives

Beyond spreadsheets, debt is a lived reality with consequences for human decisions.

Doctors delay home purchases, stretch childbearing plans, and accept positions they might otherwise refuse because loan payments demand security.

Debt contributes to the drift of physicians into employment models that offer loan assistance and guaranteed incomes at the expense of autonomy, like hospital employment, private equity-run groups.

There are social costs, too. Debt discourages candidates from low-income backgrounds and underrepresented groups, and policymakers worry that new federal borrowing constraints will worsen that trend. The physician shortage projections for the next decade (86,000) will be compounded if competent applicants self-check out of medicine for economic reasons.

This is the moment for practical clarity rather than platitudes. If you are in training or about to enter a loan-load environment, here's how you can cope:

Model several “what if” scenarios for your debt like: conservative income assumptions, deferred repayment during training, and an aggressive repayment path as an attending.

Always preserve documentation. Employment certification forms, servicer correspondence, and payment records matter enormously for PSLF.

Keep an eye on refinancing markets, but avoid refinancing federal loans before you are certain you won't need federal protections.

Negotiate loan assistance when you can. Hospital systems increasingly use sign-on incentives like retention bonuses and direct repayment benefits.

Finally, think of lifestyle tradeoffs as deliberate investments. By paying aggressively early in your attending career, you can buy financial freedom. By stretching repayment, you can buy liquidity now, but that often costs more over time.

Student Debt Policy Updates

The federal student loan landscape is shifting underfoot in 2025 in not-so-subtle ways. New legislation, administrative slowdowns, and structural overhauls are reshaping the cost and calculus of medical education in America.

For doctors and doctors-in-training, these policy tremors could redefine how long it takes to pay off student loans, what programs still offer relief, and who shoulders the greatest burden.

The federal loan system is turning into unfamiliar terrain, making even the best of us feel lost and confused.

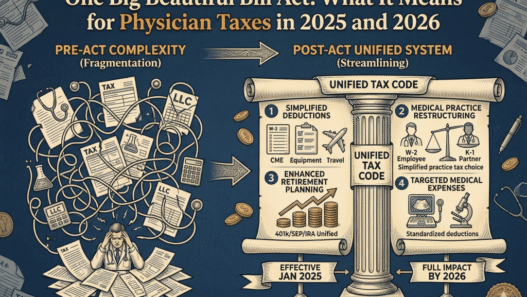

The One Big Beautiful Bill Act

On July 4, 2025, President Trump signed the One Big Beautiful Bill Act (OBBBA) into law, which is a sweeping overhaul that directly affects graduate and professional borrowers, including physicians, dentists, and veterinarians.

The most consequential change is the elimination of Graduate PLUS loans beginning July 1, 2026, which had long served as the financial backbone for medical students after they exhausted unsubsidized Stafford loans.

Under the new cap, future medical students will be limited to $50,000 annually in federal borrowing, with a lifetime ceiling of $200,000 for professional degrees.

That may sound generous until you consider that the median cost of attendance for medical school sits between $286,454 (public school) and $390,848 (private school).

The math just doesn't work like it used to. The result will likely be a surge in private loan reliance, and, by extension, higher interest rates, tighter underwriting, and fewer safety nets for borrowers who hit hard times.

Even more disruptive is the removal of residency and fellowship years from Public Service Loan Forgiveness (PSLF) eligibility.

While physicians working for nonprofit hospitals or academic centers after training may still qualify for forgiveness, the years spent in residency or fellowship (typically between three and seven) will no longer count toward the required 120 qualifying payments.

For doctors following this path, it effectively adds half a decade or more to their forgiveness timeline.

In case you missed it: The Hippocratic Divide: How the “Beautiful Bill” Fractures American Healthcare

SAVE and Other Income-Driven Repayment Plans

The same legislation also eliminates the SAVE, PAYE, and IBR programs, consolidating them into a single Repayment Assistance Plan (RAP).

RAP remains income-driven but introduces two key differences: no cap on monthly payments, and interest accrues in full. The interest subsidies that once kept balances from snowballing, particularly for residents earning under $70,000, are now gone.

As of August 1, 2025, borrowers enrolled in SAVE began accruing interest again, ending a critical benefit that helped prevent their balances from ballooning during low-earning years. The loss of that protection means higher total repayment costs, even for those who remain in good standing.

The Effect of the Government Shutdown

Compounding the disruption, the federal government shutdown that began on October 1, 2025, has paralyzed much of the administrative machinery behind PSLF and IDR programs.

While payments and disbursements continue, the Department of Education is operating with minimal staff, causing significant delays in PSLF certification, IDR recertifications, and forgiveness approvals.

For physicians who reached their 120-payment milestone this fall, that could mean months of waiting for official discharge, while still being required to make payments.

Borrowers are urged to continue paying on schedule, document every communication, and expect extended backlogs even after the government reopens.

Policy, Supply, and What They Mean

We can't separate individual financial choices from policy shifts.

The federal borrowing cap and elimination of Grad PLUS loans fundamentally change who can afford to train as a physician.

On the margin, more students will turn to private lenders, increasing financial risk, reducing access to forgiveness, and likely pushing the cost of training higher for those without family wealth or institutional support.

That dynamic has downstream effects. Fewer applicants from low-income backgrounds are expected to pursue medicine, while interest in higher-paying specialties will intensify. More physicians will accept employment contracts that include loan assistance in exchange for reduced autonomy.

At a time when the U.S. already faces a projected shortage of up to 86,000 physicians by 2036, debt is just as much of a public health issue as it is a professional issue.

Student Debt Isn't the End of the World

If you are sitting with six figures of student debt, know this: the number is large, but it is navigable. The correct response is not denial, nor is it panic. It is strategy.

Understand your likely lifetime earnings in your specialty, choose a repayment path that matches your professional plans (and keep records), delay refinancing until your career path is settled, and leverage every available employer or public benefit you can find.

But also be clear-eyed about policy changes that can blindside even the most prudent planners. A generation of future doctors will borrow under different rules than yours did, and those rules will reshape who becomes a doctor and where they practice.

We believe medicine must remain open to talent from varied socioeconomic backgrounds, but ensuring that requires institutional, legislative, and professional work, collectively.

For now, debt is heavy, but it need not determine your future if you plan deliberately and move with both humility and purpose.

Frequently Asked Questions

What is the average medical student debt for doctors as of 2025?

Among new medical school graduates who borrowed, the average debt (for the medical-school portion alone) is approximately $216,659. Including undergraduate debt, the average rises to about $246,659.

Does debt differ by public vs private medical schools?

Yes. For the Class of 2024, roughly 73% of public-school graduates borrowed, averaging around $203,606 debt among borrowers; among private-school graduates (67% borrowing) the average debt was about $227,839.

How does debt vary by specialty for doctors?

Debt interacts with specialty in multiple ways. Because income and training length vary by specialty, debt burdens can have different implications across fields.

What is a realistic payoff timeline for physician debt?

It depends on career path, income, repayment strategy and whether forgiveness applies. Many physicians who use income-driven repayment (IDR) without major forgiveness take 13-20 years. Some aggressively pay off in 5-7 years post training, but that's less common.

What major federal policy changes in 2025 affect physician student debt?

Key changes include:

- The One Big Beautiful Bill Act (July 2025) which ends Graduate PLUS loans for new borrowers and caps federal borrowing for professional degrees (e.g., $200,000 lifetime cap).

- Removal of residency/fellowship years from eligibility for the Public Service Loan Forgiveness (PSLF) required payments.

- Elimination of the SAVE Plan, PAYE and IBR in favor of a new Repayment Assistance Plan (RAP) with no monthly-payment cap and full interest accrual.

- Administrative slowdowns (e.g., due to the October 2025 Government Shutdown) affecting processing of PSLF/IDR applications and certifications.

When should a physician consider refinancing student loans?

Refinancing can make sense when you are confident you will not use federal forgiveness (e.g., not eligible for PSLF), you have stable income as an attending, and you can secure a lower interest rate. However, refinancing federal loans into private loans means giving up IDR protections, PSLF eligibility, death/disability discharge benefits and federal repayment flexibility.

What are the major pros and cons of refinancing student loans?

Pros: Lower interest rate (potentially saving tens of thousands), single loan payment, improved cash flow, flexible terms, possibility of removing cosigner, and fewer legislative‐risk concerns.

Cons: Lose eligibility for PSLF and IDR forgiveness, payments no longer tied to income, fewer protections (death/disability/forbearance), may need a cosigner, shorter hardship windows, variable‐rate risk.

How can I decide between IDR + PSLF vs aggressive repayment vs refinancing?

You will want to model each scenario: estimate your specialty income trajectory, geographic cost of living, your debt load, your employer type (nonprofit vs for-profit), and your career timeline.

Then compare:

(a) staying in a nonprofit and aiming for PSLF,

(b) aggressively repaying/refinancing if you expect high income and are not PSLF-eligible,

(c) hybrid strategies.

Running the numbers (including interest accrual, tax implications of forgiveness, etc.) is essential.

What impact does debt have on physician career decisions and lifestyle?

Significant. High debt can delay home ownership, influence specialty choice (toward higher-income fields), affect employment models (more doctors choose hospital employment with loan assistance), and delay life milestones such as starting a family. It may also discourage candidates from lower-income or underserved areas and reduce socioeconomic diversity in medicine.

What documentation should a physician keep if pursuing forgiveness or IDR?

Maintain employment certification forms (for PSLF), annual IDR certification, loan servicer correspondence, payment records, employer classification (nonprofit vs. for-profit) and any changes in employer status. Delays or missing paperwork can jeopardize years of qualifying payments.