It hit her the day the bill came.

Samantha had just landed her first “real” job — a $48k salary, a desk with her name on it, and a coffee mug she bought with her first paycheck. She was proud. Until she opened that email:

Suddenly, the weight of her degree felt heavier than the diploma frame on her wall.

Sound familiar?

If you've ever signed your name on a promissory note for college, you know the strange mix of optimism and anxiety that comes with borrowing for your education.

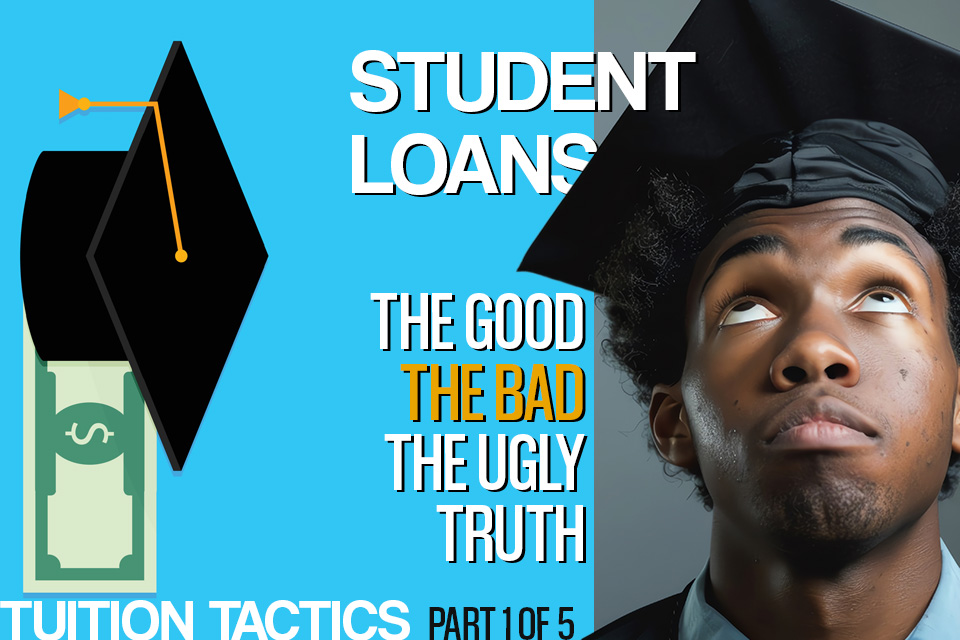

Student loans can be both a stepping stone and a stumbling block. Let's break it down.

The Good: Why Student Loans Aren't Always the Villain

Student loans are like fire — dangerous when uncontrolled, but powerful when used wisely.

- They give you access to an education you might not otherwise afford.

- They can be a solid investment if your degree leads to a career with strong earning potential.

- Federal loans offer protections — such as income-driven repayment, deferment during unemployment, and potential forgiveness programs.

If your choice is between never going to college or using a reasonable amount of federal loans to attend, loans can be the bridge.

The Bad: The Debt Creep You Don't Notice Until It's Too Late

The trouble starts when you overborrow — often without realizing it.

Here's the trap: Many students take the maximum offered each semester.

The extra money seems nice, much like borrowing more than you can afford for a nicer car or house — it “seems” nice in the moment.

That “extra” covers pizza, nicer apartments, or spring break trips. But every borrowed dollar compounds.

Example:

- Borrowing $5,000 extra each year for four years = $20,000

- At 6% interest over 10 years, that's roughly $26,645 you'll repay.

- That $1,500 laptop and a few nights out? They just cost you $6,645 in interest.

The Ugly: When Student Loans Dictate Your Life Choices

Big loans can delay life milestones:

- Buying a home

- Starting a family

- Switching to a lower-paying passion career

The numbers don't lie — a $70,000 balance at 6% interest with a standard 10-year repayment means $777/month.

That's like paying a second rent.

Federal vs. Private Loans: Know the Difference

- Federal Loans: Fixed interest rates, income-driven repayment plans, and forgiveness programs.

- Private Loans: Often variable interest rates, fewer protections, and stricter terms.

Rule of Thumb: Max out federal loans before even considering private ones.

How to Borrow Smart

- Borrow only what you need — enough to cover tuition and essential expenses.

- Do the math early — Use a loan calculator to see what your future monthly payment will be.

- Consider the ROI — If your expected starting salary is $50,000, try to keep total borrowing under $25,000 (half your first-year income).

- Pay interest during school if you can — It keeps your balance from snowballing.

Mindset Takeaway: Your Degree is a Mortgage on Your Brain

A mortgage on a home can build wealth.

A mortgage on your brain — if taken wisely — can do the same.

But just like houses, degrees can be overvalued.

Shop smart, borrow cautiously, and remember: The goal isn't just to graduate — it's to graduate free enough to live.

In Part 2, we'll dive deeper into paying for college.

The post Student Loans: The Good, The Bad, and the Ugly Truth No One Tells You appeared first on MoneyMiniBlog.